The Truth About Interest Rates and Yield Curves

In the world of finance and investments, interest rates are extremely important. As Warren Buffett famously stated, “interest rates are to finance as gravity is to physics.” As interest rates change, the value of financial assets (stocks, bonds, real estate, etc.) change. The issue is that there is massive misinformation and even confusion about why and how interest rates move.

You cannot turn on a financial news channel or read a financial news article without some mention of how interest rates are going to “pummel everything in their sight” or “cause rampant inflation” or even “start the next recession.” While any one of these can be true, they usually are not. The discussion of interest rates is much more nuanced than the talking head on XYZ financial network would like you to believe. Our intention is for you to gain a better understanding of interest rates and the yield curve after reading this article. Let’s dive in a little deeper into the topic, shall we?

As mentioned above, interest rates are really important. The prevailing interest rate environment determines how much interest we pay on our mortgages, car loans, student loans, and any other loan of which you can think. Interest rates also determine at what rate corporations can borrow to invest in and grow their business. They also determine the type of yield investors and depositors can earn on the hard-earned funds that they lend to banks and/or corporations for a finite period.

So, what exactly are interest rates? While interest rates are talked about as one entity, there are many types of interest rates. There is the federal (or “fed”) funds rate, the 10-year Treasury rate, the rate one receives on a 6-month CD at the bank, and there is a rate at which banks pay depositors on their savings/money market accounts to name a few. However, when investors talk about the Fed raising or lowering interest rates, they are only talking about the fed funds rate, an important distinction.

The fed funds rate is known as the short rate. The Federal Reserve (or “Fed”) is America’s central bank, and the Fed is responsible for setting America’s short rate. Other countries have their version of the Fed. Europe has the European Central Bank, also known as the ECB. Japan has the Bank of Japan. A country’s central bank has exclusive power on setting its country’s short rate. The Federal Open Market Committee (FOMC) meets about every 6-7 weeks to discuss if they should raise, lower, or hold the fed funds rate. The fed funds rate is also the rate at which banks lend to each other on an overnight basis.

Federal Funds Interest Rates Over the Years

The other benchmark interest rate that is often talked about is the 10-year Treasury rate. A 10-year Treasury Bond is often referred to as “the long bond.” Hence, the rate of a 10-year Treasury is known as the long rate. This rate is not set by the Fed, but rather by market forces. The market also sets the interest rate paid on the maturities of many other government bonds, from bills with 3-month maturities to bonds with maturities of 30 years.

As you may have been able to surmise from the above two paragraphs, the short rate and long rates move independently of each other. Again, this is a very important distinction (and is not known by many investors). Therefore, from this day forward separating the short rate and long rates in your mind is a great practice. You now know that using the term “interest rates” is confusing and not necessarily proper as this term wrongly lumps two independently moving entities together.

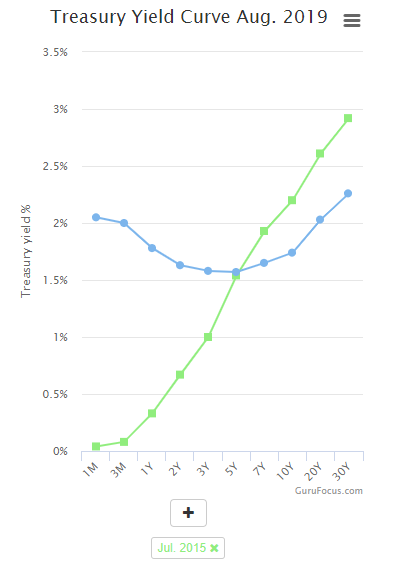

Finally, let’s move on to the application of differing interest rates to what is called the yield curve. The rates of shorter-term Treasury bills and longer-term Treasury notes are what are plotted on a graph to form the yield curve. Below is a traditional yield curve (as of July 2015, in green), and the current yield curve (in blue):

Typically, shorter-term rates are lower than longer-term rates. The reason being that bonds, loans and other financial securities with longer-term maturities usually have to compensate their holders with higher interest rates due to the additional interest rate risks associated with locking up money for longer periods. However, as you can see in the recent graph, the current yield curve is “inverted” in certain places. An inverted yield curve means that some shorter-term rates are higher than some longer-term rates. Inverted yield curves are typically signaling a bearish outlook. Why is that?

According to Ken Fisher, in his book The Only Three Questions That Count, a traditional yield curve, as seen earlier, is typically emblematic of an environment in which financial institutions can lend profitably. An inverted yield curve creates the opposite incentive. Therefore, an inverted yield curve reduces liquidity and has served as a reasonably reliable predictor of recessions. In other words, an inverted yield curve can be signaling that trouble may be on the horizon in the relatively near-term.

Of course, timing is everything. Just because the yield curve inverts, it does not mean there is going to be a recession and/or a bear market. And, even if one does occur, predicting when it will occur is extremely difficult. Further, a recession, or bear market, can be priced into the market. If a yield curve inversion is widely expected by the majority of market participants, this anxiety may cause the inverted yield curve to lose its influence in triggering a major market decline.

Due to endless speculation on the direction and level of interest rates, the Federal Reserve has been thrust into the spotlight. The purpose and power of the Fed can be questioned. Is it the Fed’s role to keep the economy expanding and keep financial asset prices ever-increasing? The stated role of the Fed is to strive for maximum sustainable employment and to keep prices stable. There is even debate around what “full employment” means and which inflation rate is consistent with price stability. Most economists agree that full employment is met at an unemployment rate between 4-5%, and the Fed has agreed upon an inflation target of about 2%. Many investors and economists believe the Fed is keeping interest rates artificially low, which has led to excessive financial asset price increases.

In conclusion, while not an exhaustive article on the subject, we hope the above dialogue on the topic of interest rates helps to put into context the nuance around the material. If you would like to continue the conversation, please reach out to your advisor or any member of the Wolf Group Capital Advisors team.